On the occasion of International Women's Day, Vibha Padalkar, ED and CFO, HDFC Life, offers a five-step plan for urban women to attain financial freedom.

On the occasion of International Women's Day, Vibha Padalkar, ED and CFO, HDFC Life, offers a five-step plan for urban women to attain financial freedom.

Why women should plan? Are women’s financial needs different?

Women face a number of unique risks -- longevity, gender-related illnesses, care giving responsibilities, ageing single, greater healthcare costs etc. And when it comes to money and investing, women have unique financial needs.

The social structure places greater burden. Pregnancy comes with its own joy and financial changes. Most opt out of career, or settle down for low paying jobs to balance career and motherhood. Many face complications, which leaves them emotionally and financially drained. Mothers often take prolonged leave of absence from their careers to take care of kids or ageing parents, which may deplete their income source and the savings gap may take years to recover.

Women’s genetic and biological makeup makes them vulnerable to medical and health situation that are unique. They bear higher risk of cervical and breast cancer. These silent killers are known to target at least 1 in 10 women, as per reports. Medical advancement has made these illnesses less severe but the financial drain of fighting these diseases is sufficient to wipe out a lifetime of savings of entire family. It’s advisable that women pay attention to their health at all time and plan proactively to build a fund that can aid in such situations.

With new demographics and social changes, women can be single through widowhood, divorced or choosing never to get married. They are, therefore, more likely to be solely responsible for their own financial independence at some point in their lives.

Though saving systematically comes naturally to women and enables them build up a disciplined approach towards investing, studies show that most don’t start saving early. Building an asset and aiming to be self reliant, sufficient to last these possibilities, requires right financial planning.

HDFC Life Value Notes Life Freedom Index reveals that only 22 per cent of urban women have a comprehensive financial plan to cover all short and long term goals while 42 per cent of them have only a basic plan, which covers only few short and long term goals, the survey revealed. In fact, only 13 per cent of urban women are extremely confident about the adequacy of their financial plan to meet all their lifetime needs. The survey was conducted among urban women in 11 Indian Tier 1 and Tier 2 cities.

What are the steps to right financial planning for a woman?

Step 1: Defining the objective

Women should clearly set a realistic financial objective, which could be purchase of home, building a kitty for post retirement income, starting a business, overseas travel, buying a car, creation of fund for child’s marriage, education etc. Defining the amount of money and the time horizon for accomplishing the objective is the second important factor, as it determines the choice of investment instruments and impacts the accomplishment of the objective.

Step 2: Preparing a plan

A financial plan starts with income and expenses and projecting future expenses and income. This gives a fair idea of what amount is required to meet various current and future financial objectives. Various factors such as time horizons, risk appetite, and type of investment avenues available are also considered. It’s important to build some form of contingency plan, so that savings can continue even in case of unforeseen circumstances like illness, death of spouse or loss of job. Because women are more likely to have work disruptions for care giving, they need to capitalise on savings opportunities while they are working, in order to compensate for a longer average longevity.

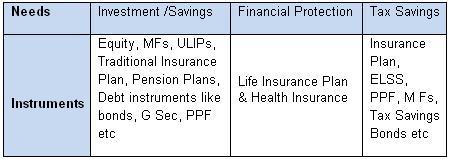

There are many instruments that fit the diverse needs. A snapshot of these instruments is mentioned below:

Improper diversification of financial assets may limit the potential to generate sufficient income from a portfolio and allow inflation to reduce the portfolio’s purchasing power over time (and, given women’s longer life spans, the long term is critical). Over the long term, shunning equity in favour of bonds can mean a portfolio isn’t properly diversified and so may not combat the eroding power of inflation. Consulting a certified financial advisor is advisable for the right approach to a financial plan.

HDFC Life ValueNotes Life Freedom Index reveals that Indian urban women score low in financial awareness (44.4 on a scale of 0-100) of various life events (expected and unexpected) and products. There is a glaring gap between product knowledge (61.6 on a scale of 0-100) and event awareness (27.4 on a scale of 0-100), which implies that the products she invests are not according to her financial requirements.

Step 3: Starting to invest

Disciplined investment is the key towards success of a financial plan. Today, most of the investing can be done online. Most financial advisors help in documentations. However it’s important to read and understand the nature and associated risk of each investment instrument, before investing.

Step 4: Reviewing plan periodically

Once investment starts, to ensure that you stay on the course, it is advisable to review them in line with increased income or expense, new assets or liability acquisitions or changing market conditions. For example, plan should be reviewed to judge the performance of various investments. When stock markets change course over a period of time they may disturb your asset allocation. So you may have to redeem some of your equity investments or buy more of them depending on how much risk you are willing to take.

As you approach the milestone (child's college admission or marriage), you would need to get out of equity investments and move to debt to protect your accumulated funds.

Step 5: Redeeming investments

As the milestone you have been saving for approaches near, you would need to redeem your investments. In case of a life insurance policy, it involves submitting your policy documents to the life insurer and follow up for the maturity proceeds. You may also need to sit down with your financial consultant and understand the taxation issues involved with the redemption of your investments (if any).

What are the things women should keep in mind while opting for insurance?

Women should be educated to avoid common mistakes of considering insurance as a low priority and focusing less on health insurance. They also need to be made aware of the perils of relying too much on relatives and friends for investment advice.

For married women, it is important to understand the level of insurance cover that may be required to cover benefits, current income including living expenses, education expenses and retirement benefits. A plan like Smart Woman can play a big role here.

If she has taken a career break, she may go for affordable protection plans with specific rates for women to continue life coverage during income disruption periods at a minimal cost. Alternatively, single premium term plans can also be helpful. The approach should be to go for optimal risk cover with some investment for long-term savings. It is important to note that long-term savings does not require an individual to pay high premiums, but it requires payment of affordable premium for longer duration.

Working couples should look at their current expenses and long-term goals and buy an insurance product to cover their liabilities. When a woman gets married or when other life milestones are reached, she should update her basic policy details, such as updating of name, nomination and new address. If she has too many liabilities, protection plans can provide the funds to pay off debts, such as home mortgage, in the event of the borrower’s death. These plans also offer joint life or co-borrower cover.

Know your life cover: Every married woman should be aware of the basic information, such as a legal Will, if any, insurance policies or other investments made by her husband, contact details of the financial companies from where investments have been made and bank account details to which claim amount should be deposited. She should also be aware if the spouse has bought a life insurance policy under MWP Act.

Why women should invest time in financial planning and take informed decision and not leave it to others?

HDFC Life Value Notes Life Freedom Index reveals that close to majority (42 per cent) of Urban Women chalk out their financial plans with the help of their friends and relatives, only 26 per cent consult financial planners and advisors in the financial planning process.

It is important to understand that just as every woman spends hours to figure out the right kind of outfit, kitchen appliances, holiday packages, etc, it is equally critical to invest time to educate about the different investment vehicles available along with the different life stage events for right approach to financial planning. Women should cultivate a habit of reading different personal finance columns, and related publications to brush up knowledge on finance. Women must know what exactly they are investing in. They should not blindly follow others advice. Only an informed mind can take the right decision.

After all, you must carve and decide your own financial future! This would help you to maintain your ‘self respect’ and ‘self dignity’ irrespective of the outside environment.