Here's what's in it for you!

In a competitive market, companies go beyond offering core value in their products. Companies have been working towards product customisation to match the product offering with the customer requirement and needs, and credit cards are no different.

Considering the broad range of credit cards offerings in the market, we see that these have evolved from mere tools providing cashless transactions to complex tools where customers can 'earn' by spending more! Over a period of time, credit cards usage has gained grounds, but cash continues to remain important.

What you get in return for purchases you make using cash back credit cards? The answer is 'cash rewards'.

The cash back credit points have gained popularity in recent times. These cards allow the cardholders to earn 'cash rewards' for making purchases with their credit cards. Usually, the cash earned on the cash back cards is around 1 per cent of total purchases, which excludes the interest and finance charges.

There are many cash back credit cards available in the market today.

For example, HDFC Women's Gold Credit Card provides as much as 5 per cent cash back* on all grocery and medical purchases.

(* Subject to condition that the statement balance for that month is above Rs 20,000. Cardholders can earn up to Rs 1000 as cash back per month, which is credited to the card account in the subsequent month.)

The Citibank Cash Back Credit Card holders can earn Re 1 as cash back for every Rs 200 spent using the card. These cash back earnings can be redeemed once the more than Rs 250 cash back are earned.

The ABN-AMRO One Credit Card offers cash back on all types of purchases. The card offers 1 per cent cash back on monthly spends up to Rs 5000. The cash back on monthly spends between Rs 5,000 to Rs 10,000 is 1.5 per cent. On purchases above Rs 10,000, the card offers cash back of 2 per cent. The maximum cash back that can be earned in a month cannot exceed Rs 500, which is Rs 6,000 on annualised basis. The card also offers cash back of 1 per cent on international retail and cash transactions and 2 per cent on utility bills payment made using the bank's Smart Pay payment facility.

The Standard Chartered Business Gold Card offers 5 per cent cash back on Fuel and Telephone Bills and 1 per cent cash back on all other ransactions.

The HDFC Gold Business Card for self employed people offers exclusive privileges on business allied spends made by the cardholders. The card brings cash back rewards 1 per cent each, on air-tickets and utility bill payments. The card also offers surcharge waiver on railways and petrol expenses.

Calculating cash rewards gains on your card

You can calculate the cash rewards benefits you can draw on your credit card. For example, if you end up paying an average of Rs 25,000 credit card bill on monthly basis, then using an appropriate credit card, you can earn cash back on your card.

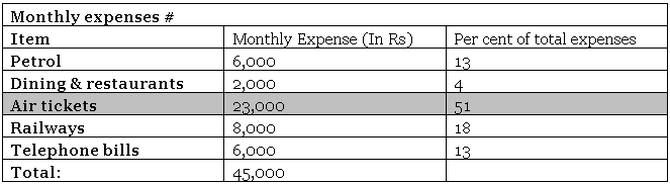

Let us understand this with an illustration. Suppose your monthly expenses are as follows...

Using an appropriate cash back credit card, you can save on each of these expenses, as shown in the table below:

# The above figures are hypothetical expense estimates.

From the table above we find that travel by air and railways both constitute major expenses. The air travel expenses are as much as 51 per cent of the total monthly expenses. On basis of this, one should analyse the monthly and recurrent expenses and choose a card that offers maximum value (in form of cash rewards) on your spendings.

It is important to note that cash rewards are not the same as cash. When a card company entitles you to cash rewards, it is not extending liquid cash in hand or in you bank account. The cash rewards are credited in the 'card account' and can be adjusted against the future payments on the card.

![]()