Photographs: Rediff Archives

Have a query regarding mutual funds? Maybe we can help.

Drop us a line and our expert, Anil Rego of Right Horizons, will answer it.

Got a question for Anil Rego? Please write to us at getahead@rediff.co.in with the subject line as 'Mutual Fund query'.

I started investments when the markets were on a bull run, however, now all my investments are in the red. I have been investing through the systematic route, should I continue investment or stop?

I am part of a new company which has only 4 executives. In my compensation there is a provision of 15 per cent of basic pay as superannuation fund contribution, but sadly I do not know any fund which allows deposit of this contribution particularly when employee strength is less than 10. In this case please let me know whether this contribution can be deposited in any fund which will give me moderate/decent return. I can cash out also but from I-T angle it is not beneficial because I fall in the 30 per cent bracket. I have already accumulated about Rs 1,10,000, so pl. advise about the scheme which allows single premium also besides monthly premium.

Thanks, Laksmi Narayanan

Dear Lakshmi Narayanan,

There are multiple options that one can avail, if you have not completed your section 80C benefit, it is suggested that you look at availing this benefit wherein the maximum limit is Rs one lakh -- you can choose to invest in conservative options like PPF, 5-yr Bank FD, NSCs, traditional insurance, etc. Part of the investments can be in market linked investments like ELSS (Tax saving mutual Fund), ULIP/ Insurance -- all these investments would qualify for tax benefit, further the maturity amount will also be tax-free. ELSS and ULIP/Insurance will offer the single payment mode as well as monthly mode for investment.

Dear Anil,

One of my relative is looking to invest around Rs 50,000 in a breakup manner such as 10,000, 15,000, 12,000 etc in a different lot for a period of six year for the purpose of marriage if his daughter, so requesting you to please suggest the best MFs in which they can invest for this period in a small lot of money as mentioned above.

Regards, Farrukh Nadeem

Dear Farrukh,

Considering that the need is conservative, I would suggest predominantly using Balanced Funds like HDFC Prudence and SBI Magnum Balanced. Over the next 2-3 years, your relative can look into investing in some good large cap diversified Equity Mutual Funds like HDFC Top 200, DSP Blackrock Top 100. If one does see some good returns, profit booking to debt funds can be considered. As one gets closer to the need, it is suggested to move the portfolio into debt so as not to be impacted by market volatility.

One can also invest in ULIPs with a balanced fund option if one would like to take care of life cover as well.

Hi,

Good Morning

I would like to invest around 60,000 rs in mutual fund. Please suggest me some mutual funds where i can have good return and tax savings.

Regards,

Deepak

Dear Deepak,

For tax saving point of view we suggest investment in:

- HDFC Tax saver

- Sundaram BNP Paribas Taxsaver

- SBI Magnum Tax Gain

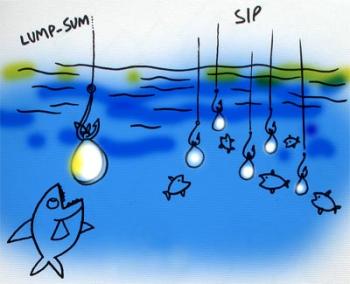

However, we suggest you to invest via Systematic investment; this method will help you avail the benefit of cost averaging. It is also an ideal way to gain exposure into equity mutual funds.

Hi Anil,

My age is 29 years and I have taken two MF 'Maximiser (Growth) Fund -- Life Time Super' and 'Pension RICH Fund -- LifeStage Pension' from ICICI Prudential, from which Maximiser will mature (3-year lock period) with returns of 26 per cent on total investment in three years.

My question is: Should I continue with the policy and pay premiums for long term?

Please note that these are not mutual funds. These are ULIPs. ULIPs ideally work well over the medium to long term. Hence, it may be imprudent to evaluate them over periods ranging between 3 to 5 yrs. It appears that someone has mis-sold the product. No ULIP guarantees a 26 per cent return.

Also initial charges are highest in the first 3 years and hence it works better for longer holding periods. Since you have already taken the plan, it is suggested that you hold both the plans for the long term 6 to10 years at least. Please note that pension plans are taxable.

Should I stop paying the premiums but let the money invested for better returns?

You can pay premiums for the minimum period of 3 yrs for Life Stage Pension. However, it is not suggested that you surrender the policy- it can be kept for the long term. Life stage Pension can be exited after about 5-8 years. Going forward, it is advised that you look at your investment objective / financial goals and conduct investments inline with the long-term goals.

Simply take out the money and invest in better plans.

The premiums which were being routed into pension plans can be used towards investment in diversified equity mutual funds since, it seems like your objective at this stage is only potential upside. You can choose a combination of midcap and largecap funds.'Domestic markets could see a significant upside'

I want to know if there is any fund in India giving the opportunity to invest in international markets? Is it advisable to start invest in international markets right now?

Thanking u, Sir.

S Jagadeesh Kumar

Hi Jagadeesh,

There are few funds that give the opportunity to invest in international market like Birla Sunlife International Equity, Fidelity International Opportunity, SBI Magnum Global Fund etc. JP Morgan has a China focused fund and Franklin Templeton has an emerging market focused fund. Indian economy looks more promising over the medium to long-term the growth story of domestic markets is expected to be phenomenal over the next 5 to10 yrs as compared to developed markets.

There is considerable growth opportunity in cCinese economy as well. There are a slew of investment opportunity in the form of new fund offers which offer exposure towards the 2 growth stories India and China. At this point it is suggested that you consider investment into domestic markets, there could be significant upside over a 3 to 5 yr period.

Dear Sir,

My fixed deposit matured recently. Should I continue with interest of 7 per cent per year or invest in mutual funds? I would like to invest Rs 10000 per month in mutual funds if it fetches better returns than FDs? Please suggest 10 SIP funds for the period of 3 years.

Please kindly reply: Rajkumar S. Verlekar

Dear Rajkumar,

Fixed deposits and equity mutual funds are not comparable, since they are two different asset classes. FDs are low risk avenues and equity mutual funds are relatively high-risk avenues, when the risk levels are high, the possibility of potential upside is also on the higher side.

Within the world of low risk avenues, instead of fixed deposits one can look at fixed maturity plans which are more tax-efficient. Returns from fixed deposits are taxable at normal rates (up to 30.9 per cent); FMPs would be taxed at a maximum of 10 per cent if held for a year.

If you are willing to assuming a higher risk profile, then we suggest you to invest in equity mutual funds which will offer potential upside. The SIP route is a preferred option as it manages risk as well. You can look into investing in some good large cap diversified equity mutual funds like HDFC Top 200, DSP Blackrock Top 100 or midcap funds like Pru ICICI Discovery Fund, SBNPP Select Midcap, HDFC Top 200

We do not suggest you to spread across 10 funds, since this would lead to gross fragmentation, complicating manageability of portfolio.

Sir, I want to invest Rs 75,000 in 5 funds for at least 3 years. Please suggest at least 5 balanced funds.

You can look for HDFC Prudence, SBI Magnum Balanced, Birla Sunlife Balance and DSPBR Balance Fund for investment from 3 yrs perspective. Given the time horizon of 3 yrs, you can also look into few of the large-cap equity diversified funds like HDFC top 200, DSP Blackrock Top 100.

Dear Anil,

I have following portfolio with me.

ICICI Prudential Dynamic Plan (D): Rs 1,000 SIP

Hold

Reliance Growth (G): Rs 2,000 SIP

Can switch to Reliance Regular Savings Equity Fund a better fund within the same genre / AMC

Birla Sun Life Infrastructure Fund (G): Rs 2,000 SIP

We suggest you to stick to diversified equity funds at this stage, hence you can stop this SIP and consider investment in Birla SL Midcap Fund (Century SIP) which will also offer cover alongside potential upside.

Fidelity Equity Fund (G): Rs 1,000 SIP

Hold

Reliance Natural Resources: Rs 30,000 lump sum

Exit and consolidate within Reliance Regular Savings Equity. We are not bullish on this fund / sector. Also, we choose to invest in diversified equity as compared to sector funds.

Tata Indo-Global Infrastructure Fund (G): Rs 25,000 lump sum

It is a lock-in fund and we suggest that on maturity, you can move the proceeds into a diversified equity mutual fund after the lock-in period. Ideally you can avoid sectoral funds.

Birla Sun Life International Equity Fund -- A (G): Rs 25,000 lump sum

Consolidate within Birla SL Midcap Fund, we are bullish on domestic markets as compared to international markets. Hence, suggest investment in funds which scout for domestic opportunities as compared to funds which are focused on international markets.

Is the above portfolio is OK considering 3 years of investment for the return of 15 per cent and above?

You can re-align your portfolio based on the above suggestions, a 3 yr horizon from here is appropriate to expect an average of 15 per cent returns from equities. Do book profits at intervals in case of a market run up.

Please suggest any additions/deletions in the above portfolio.

You can add Sundaram Select Midcap Fund (Midcap Fund) and HDFC Top 200 Fund (Large Cap Fund).

Thanks and regards,

Rajesh Khair

'For your son's education you can use a children's plan ULIP'

Dear sir, I am 28 and my portfolio is as follows:

- Sundaram tax saver (D): Rs 2,000

- DWS tax saving(D): Rs 2,000

- IDFC Imperial equity: Rs 1,000

- DSP BR Top 100: Rs 1,000

- ICICI Pru Infrastructure(D): Rs 2,000

I have withdraw 16k from DWS Alpha Equity and adding amount to 25 k and planning it to invest in Birla Frontline Equity Plan in STP form (weekly 1k). Can you please suggest if my decision of selecting funds is a good one?

Thanks, Aishwarya Koche

Dear Aishwarya,

You can exit from DWS Tax Saving and IDFC Imperial equity and invest in Birla Sunlife Midcap Plan, HDFC Top 200, DSPBR Equity. For the lump sum investment, I think the STP route is a good idea. Since you are being conservative and using the STP route and averaging out your investment, you can use a midcap fund like Birla Sunlife Midcap.

Hi Anil,

I would like to invest for my son's education, which is required after 10 years. Please let me know the good options for doing that, with MF or ULIP or else? I also want to invest for retirement for 20 years, which scheme is better for that.

Regards, Mohan

Dear Mohan,

You can invest in a combination of ULIP and mutual funds. Within mutual funds you can look at building a portfolio with moderate risk profile. ULIPs will prove to be fruitful whilst looking at a term ranging over 6 to 7 yrs. We also suggest you sketch an elaborate plan with appropriate asset allocation which will provide optimal risk-adjusted returns in the long run. Build a plan which has the right debt-equity mix.

For your son's education need considering the conservative nature of the need, you can be a little conservative and even use some debt options. On your retirement you can take a higher risk.

For your son's education ULIP, you can use a children's plan ULIP/traditional insurance plan that covers your life and provides a second level of security to this important need. For your retirement you can use a whole of life ULIP. For the mutual fund portion you can use a combination of large cap and midcap funds that you can invest through a systematic investment plan (SIP).

Hi Anil,

Is buying a gold ETF equivalent to buying gold in every sense? Are gold ETFs immune to inflation?

Regards, Nishit Agrawal

Hi Nishit,

The underlying asset incase of gold ETF is units of gold, hence it is equivalent to investing in gold itself. Gold is a store of value. Hence is a good hedge against inflation. Gold as a commodity has reached significant levels and is trading much above $1000 levels, we suggest you to hold approximately 5 per cent of portfolio in gold, apart from investing ETFs you can consider investing in gold mutual funds which offer the benefit of inorganic growth by means of consolidation of mining companies etc., their growth is not solely dependant on gold price up tick, hence one can continue to see considerable gains even during stable times in the market.

Dear Anil,

I have the following investments in MFs thru SIPs for 12 months and is not active now, but amount is still invested.

1. DSP BR Top 100 Equity (D): Rs 19,000

2. HDFC Equity Funds(D): Rs 26,000

3. Reliance Vision Find (D): Rs 18,000 and

4. Sundaram Select Focus (D): Rs 24,000

And right now, I have active SIPs in the following MFs:

1. DSP BR Top 100 Equity (G): Rs 5,000

2. HDFC Top 200 (G): Rs 5,000 and

3. Reliance Regular Saving Fund (G): 5,000.

I can stay invested for long periods say 10 to 15 years. I don't need this money which I invest in MFs. Please review my portfolio and suggest if there is any room for change. Also I can invest another 5,000 per month. Please suggest some other MF keeping in mind my current investments in MFs.

It would be great if you could reply to my query. Thanks you very much.

Regards, Pavnesh Kaushal

Dear Mr, Pavnesh,

Your mutual fund portfolio looks goods. You have adopted the right strategy of being defensive during market downturn and getting into slightly aggressive funds during stable times, at this point we suggest you to use one more midcap fund like Birla SL Midcap or SBNPP Select midcap. We also suggest you to consolidate your portfolio within a set of 6 to 7 funds, over a period of time, you can consider addition of approximately 5 per cent of portfolio into gold ETFs or MFs which can act as a hedge against your existing equity portfolio.'At the moment, we do not suggest exposure in sectoral funds'

Hi! I have the following investments in mutual funds. I would like to start a SIP of Rs 3,000 for my newborn child. Basically am looking at a 15 to 20 year horizon and would like to use the money for her higher studies. Please advise which fund to invest in:

Bulk investment

1) ICICI Tax Plan: Rs 10,000

2) DSP Black Rock Tax saver: Rs 10,000

3) Kotak Mid Cap: Rs 10,000

SIP with monthly investment

1) Birla Top 100: Rs 2,000

2) HDFC Growth Fund: Rs 1,000

3) ICICI Dynamic Plan: Rs 1,000

4) Kotak 30: Rs 1,000

5) HDFC Top 200: Rs 2,000

Regards, Gurveer

Dear Gurveer,

For SIP you can look into any of the child benefit plan, this will be a balanced fund, and conservatively managed. Given the time horizon of 15 to 20 years, you can also look at availing a child plan which will help you to plan this need with a 'Low-Moderate' risk profile, there are plans which offer payouts as per the milestone of the child, they will also offer hedge against eventuality by providing the waiver of premium option which will essentially mean that incase of eventuality of parent, the plan will still continue unperturbed and the payouts will happen at appropriate milestones.

We suggest you to consolidate your SIP investments within a set of 3 funds, essentially with a midcap bias. We suggest the following funds for the SIP:

- Birla Sunlife Midcap (Century SIP)

- HDFC Top 100

- ICICI Pru Discovery

I have invested in monthly SIP in the following funds:

- Magnum Contra

- Magnum Tax Advantage

- Reliance Diversified Power

- Reliance Growth

- Can Rebecco Equity Tax Saver

- DSP Blackrock Tiger Fund

- ICICI PRU Discovery Fund

In all the funds it is growth Option and I have invested in these funds keeping in mind long-term horizon of 5-10 years tenure.

Please let me know whether the funds selected are perfect or I need to re-shuffle the portfolio.

Thanks, Arindam

Dear Arindam,

Broadly your choice of funds are good, we suggest you to consolidate Reliance Div Power and Growth within Reliance Regular Savings Equity Fund. At the moment, we do not suggest exposure in sectoral funds, further it would be more rewarding to stick to a fund with an essential midcap bias at this point, we suggest moving towards a fund which has a good track record and the composition to clock some decent returns within the genre / AMC given the current market trend. (HDFC Top 200 / Sundaram Select Midcap fund)

'It's inappropriate to evaluate ULIP returns over a shorter horizon'

Dear friend,

I had invested in Market Plus of LIC to the tune of 15 lakh. I find there are not much appreciative returns. I am serious thinking of withdrawing and invest in a good mutual fund. Will you please advise me as to how to proceed in the matter?

O.N. Umashankar

Dear Umashankar,

Market Plus is a ULIP, it may be inappropriate to evaluate ULIP returns over a short horizon (within 3 yrs), however, given the voluminous investment made, we suggest you to evaluate the losses and based on this you can consider exiting the investment in full or even partially. We suggest that you evaluate the product in detail, inline with your financial goals and based on the same deploy funds.

Whilst investing in mutual funds also, spare a thought on how you would like to design your portfolio, have a heady mix of debt / equity. Also, ensure that it is well within your risk profile and is manageable from the perspective of re-alignment based on market trends. You can also choose to invest a part into ULIPs where in the charges are more staggered in the long run, further you can choose one with good returns in the recent past.

Hi, my query is:

I've no prior experience in stock/mutual fund. I'm planning to invest in mutual fund for saving/growth purpose. I can invest 2 to 3K per month targeting for 3 year. Please suggest good mutual fund schemes.

Thanks, Prajesh

Dear Prajesh,

You can invest in SIP of HDFC Top 200, Birla Sunlife Midcap Plan. Incase you have not planned for section 80C then you can choose to invest in Sundaram BNP Paribas Taxsaver or SBI Magnum Tax Gain.

Hi,

I am planning to invest Rs 10 K on monthly basis in mutual funds. Do I need to invest Rs 10k in one fund or diversify it. If I put my money in different funds, individual fund provider will charge there fee right. Please suggest a plan for investing.

Thanks, Sajin

Dear Sajin,

You can probably invest 5k and 5k in two funds. You can look for Birla Sunlife Midcap Plan, HDFC Top 200. One is a midcap and the other a largecap fund, with the elimination of entry load, there will be no entry load charged on any of the funds. There is no difference in charges between 1 and 2 funds.

Dear Anil,

We have earning of approx 55k per month (22K is mine and 33k is my husband's). We have ICICI Prudential Super saver Plan of @ 3000 per month and we have a LIC of @5,000 annually also last month we have bought shares of Kaveri @ 20K. We are planning to invest/save @20K monthly. Can you please suggest any suitable plan where our money should be save as well as we can get return? We want one retirement plan also.

Regards, Pooja Kumar

Dear Pooja,

We can look at a diversified approach for the investible surplus, you can consider a whole life endowment unit linked plan which can be made to work like a pension scheme. We do not suggest investment into a pension scheme since the payouts will be taxable.

Whilst investing in mutual funds also, spare a thought on how you would like to design your portfolio, have a mix of debt / equity. Also, ensure that it is well within your risk profile and is manageable from the perspective of re-alignment based on market trends.

The funds you can consider at this point are:

- Birla Sunlife Midcap Plan

- SBNPP Select Midcap

- HDFC Top 200

- DSPBR Top 100

You can also consider adding DSPBR World Gold fund which can hedge your equity portfolio. However, this can be done only after to build a decently huge equity portfolio. At this stage we suggest restricting your equity mutual funds to 3 to 5 funds only.

Dear Sir,

I am not an investor, however I want to invest now in MF thru' SIP. Amount may be Rs 2,000 pm in two to three MF. Can you advise me the best for me?

Regards, R C Thakur

Dear Sir,

You can invest in MF like HDFC Top 200, Birla Sunlife Midcap plan, DSPBR Top 100, ICICI Prudential Discovery fund, Sundaram BNP Paribas Select Midcap.

Comment

article