| « Back to article | Print this article |

Marriage and money: What not to do

A newly married friend confided in me about a problem he encountered in his marriage. He said that his young bride never told him about the debt she had incurred on her credit card and personal loan before they tied the knot. And now, her spendthrift ways have resulted in a major chunk of her salary going towards clearing it and he has to run the house on his earnings.

So his plan of taking a home loan by combining both their incomes has been shelved for now. More than the financial implication, he said he felt betrayed by her lack of honesty.

This got me thinking. How important is it to be financially compatible in a marriage?

"Very," said my cousin who is a divorce lawyer and himself happily married for 25 years. According to him, and I do trust his judgment, "the three most important ingredients in a marriage are trust, money and religion." So if money is that crucial, what must couples do to make sure they are on the same page where their spending is concerned? If there is a conflict, what is the best way to resolve it?

It all begins with a bank account

I decided to get some answers by talking to (and e-mailing) my married friends. They were pretty forthcoming and unanimous on the issue that money, if not dealt with complete openness and honesty, could bring about a huge dent in the relationship. So how did they deal with it? What you read now is just a summary of what I gleaned from their experiences.

It all begins with a bank account. All agreed that a joint account is a necessity. But what happens if both couples have corporate salary accounts? Even so, having one joint account makes sense. One of my friends said that he and his wife each put in 70 per cent of their respective salaries in the joint account and the entire household is run on that combined amount. The balance 30 per cent that each retain is used for their own personal expenses, or helping out their parents with a monetary gift and even investing in their own tax savings investments.

In this way, they combine their incomes as well as have independence.

The main focus of having a joint account is not to distinguish between 'my money' and 'your money'. It must be 'our money'. More so, when it comes to just one spouse working. For instance, does a stay-at-home mom have a say when her husband is the one who brings in all the moolah?

'I have a fairly democratic outlook in life and that makes it easier to work things out,' is from someone whose wife is a homemaker. Despite the fact that she does not contribute to the household income, he ensures that all big-ticket expenses are discussed together. They do have occasional disagreements on the small sums here and there but are open and candid when it comes to shelling out the big bucks.

'Opinions and suggestions are valuable'

A dialogue is a must when it comes to huge expenditures like a holiday. Perspectives differ, so it's essential to know the other person's thought process and reasons for wanting to, or not wanting to, spend a particular amount. "The issue at stake is that one should never take the other for granted," says a friend who earns much less than her husband.

"I may be earning less but my opinions and suggestions are as valuable as my husband's because we are in it together."

The best way out is for both to list down what they are saving for. Let's say they put down three goals: a car, a holiday, and the down payment for a home. Once that is decided upon and each given a figure and a date, the priorities are set accordingly. Sounds simple, but can lead to quite an argument.

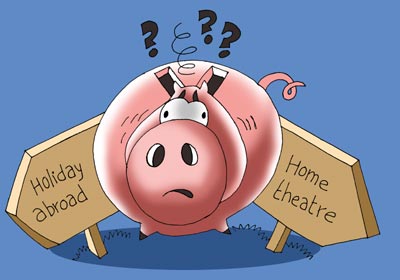

I know of a couple where the man wanted to spend on a hi-tech home theatre and LCD while his wife preferred a holiday abroad. The problem was not the goals but that both wanted their own as the No. 1 priority. They finally agreed to use their savings for the home theatre and take a personal loan to go on the holiday.

Here's how to make it simpler

Sheryl Dixit, a friend who has relocated abroad, says that she and her husband are unanimous when it comes to the big-ticket items but differ on the nitty-gritty.

"I could never understand why my husband considered expensive beer a necessity, and he couldn't understand why I spent money on waxing," is what she mentioned over e-mail. But they were pretty much in sync with what the big expenditures should be.

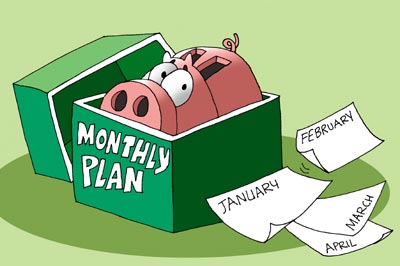

The most practical way is to work on a monthly plan. Once it's decided how much of money must be allocated to these broad areas: bills (rent, electricity, phone, mortgage), household expenses (groceries, toiletries, eating out, ad-hoc expenditure) and savings (towards all goals including retirement), it becomes much simpler.

But the key is to communicate, be open and frank. And, most importantly, when discussing or bringing up money disagreements, ensure that it is at a time when both are calm and not in the midst of a fight on another issue.